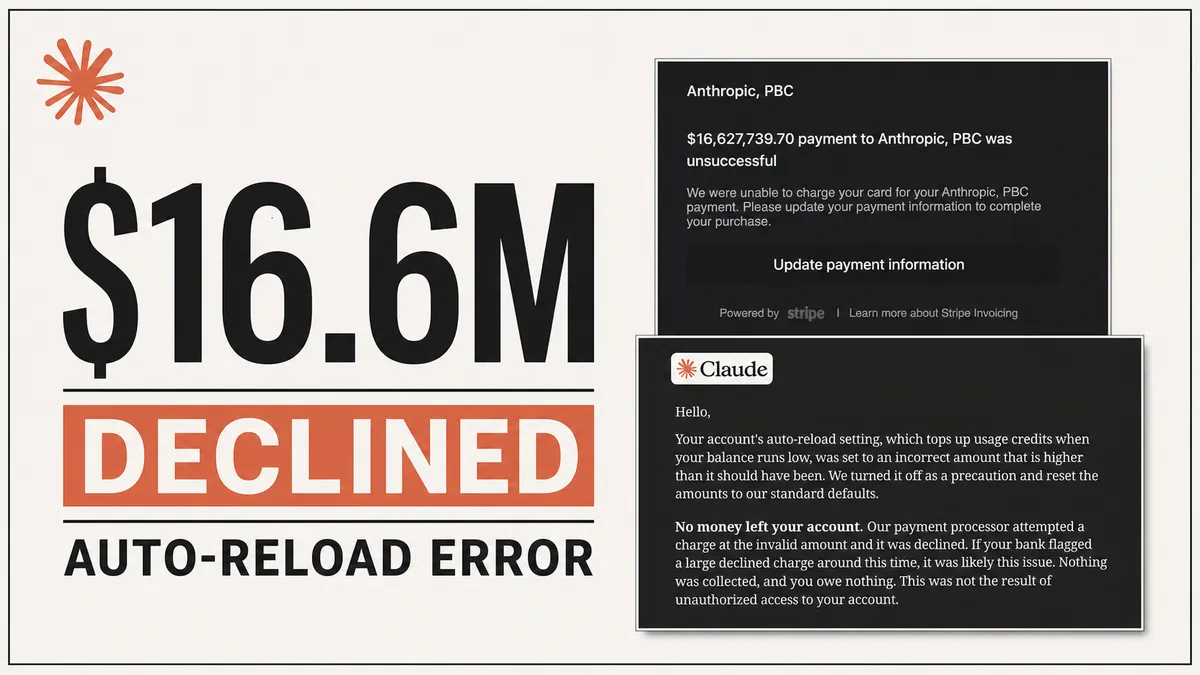

A South Korean Claude user received a failed-payment notice for $16,627,739.70 even though the Anthropic console reportedly showed $0.00 in API usage. Anthropic later acknowledged that the account’s auto-reload amount had been set incorrectly.

The money did not leave the account. The incident still escaped Anthropic’s dashboard and reached the banking system. In a follow-up account, the user said the bank received more than a dozen invalid payment attempts, the primary card became unusable, and 15 messages across Anthropic’s support, technical, marketing, and engineering channels produced only an automated escalation notice after four days.

That makes the episode more than an amusing invoice screenshot. It is a case study in two linked failures: a billing path that allowed an obviously abnormal amount to reach a bank, and an incident-response path that did not quickly put a human in front of a customer reporting an eight-figure payment attempt.

What happened

The public timeline is based on Threads updates from @remy_notes, screenshots shared by the account, Korean reporting, and a later support response attributed to Anthropic.

- On July 7, the user received a failed-payment request for $1,669,875.90.

- On July 8, another notice raised the requested amount almost tenfold to $16,627,739.70.

- The Anthropic dashboard reportedly continued to show no corresponding API usage.

- The user audited agents, scheduled jobs, proxies, and API credentials while trying to determine whether an automation had escaped its budget.

- The user says the bank received the invalid requests more than a dozen times and the primary card was blocked during the incident.

- After 15 emails across several Anthropic contact channels and four days of waiting, the user says an automated notice reported that one request had been passed to a human agent.

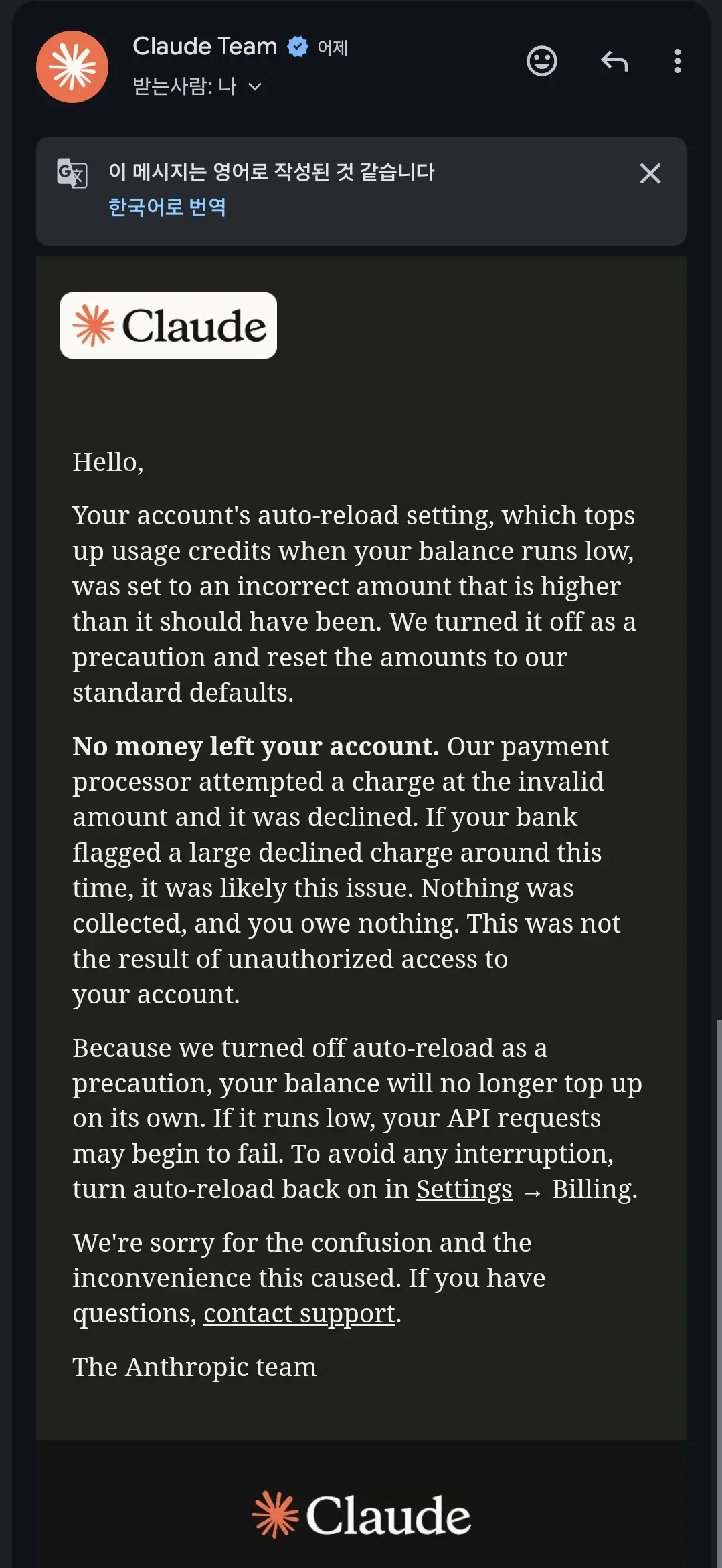

- Anthropic later told the user that an auto-reload setting had been assigned an incorrect amount, disabled the setting, and reset it to the standard default.

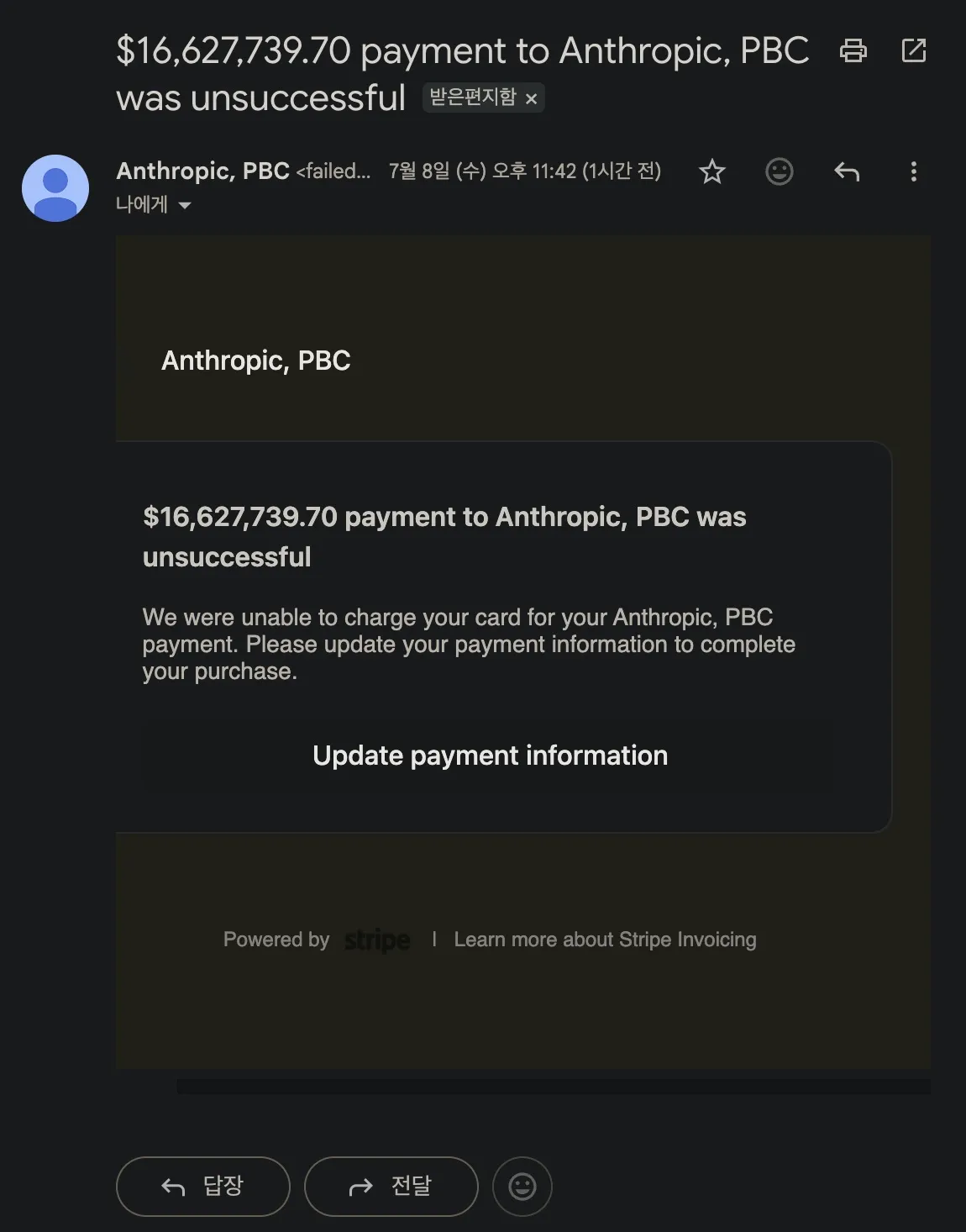

The notice records an unsuccessful $16,627,739.70 payment request. It does not show a completed debit. Screenshot: @remy_notes on Threads, supplied by the user for reporting.

The notice names Anthropic and says it was powered by Stripe rather than asking the recipient to enter credentials on an unfamiliar page. The user also said the card issuer recognized Anthropic as the merchant. Those details reduced the initial possibility of an ordinary phishing email, although checking the sender, links, and bank activity was still the correct first response.

What Anthropic confirmed, and what remains unknown

In the support email shared by the user, Anthropic said the account’s auto-reload setting was “set to an incorrect amount” that was higher than intended. It also stated: “Nothing was collected, and you owe nothing.” The company said the event was not caused by unauthorized account access.

That answer establishes three facts:

- The payment processor attempted an invalid amount.

- The attempt was declined, so no money left the account.

- Anthropic attributed the event to an incorrect auto-reload amount and turned auto-reload off.

It does not provide a complete root-cause analysis. Anthropic has not publicly explained how the amount entered the billing state, why it increased by almost ten times, why the customer dashboard and payment request appeared to disagree, or which control prevented the request from reaching a processor before the bank had to reject it.

Claims that the bug involved currency conversion, Unix timestamps, cents versus dollars, or an AI-written billing system remain speculation. They appeared in the Reddit discussion because the number looked machine-generated, not because Anthropic confirmed any of those mechanisms.

No money moved, but the failure was not harmless

Anthropic’s statement that no money left the account is financially important and factually different from a completed $16.6 million debit. It is not a complete description of the impact reported by the user.

The response says the auto-reload amount was incorrect, the processor attempted the charge, the bank declined it, and the user owed nothing. Screenshot: @remy_notes on Threads, supplied by the user for reporting.

The user says repeated attempts disrupted the primary card and created a potential credit and banking problem. That is an operational loss even when the final settled amount is zero. A payment system cannot define success only as “we failed to collect the invalid charge” if its retries trigger fraud controls or remove access to a customer’s normal payment method.

The support timeline compounds that failure. The user says 15 messages were sent across support, technical, marketing, and engineering contacts. Four days later, the only acknowledgement of human escalation was itself automated. The email corrected the account state, turned off auto-reload, and told the user to switch it back on if uninterrupted API access was required. That is reasonable containment, but it is not incident ownership: the message offered no root-cause analysis, no explanation of the repeated bank requests, and no help restoring the blocked card.

The distinction is useful for incident reviews. The financial outcome was a declined payment. The customer impact included a disabled primary card and days of uncertainty. The response outcome was a configuration reset without a timely, accountable human explanation. All three belong in the severity assessment.

Reddit moved from disbelief to a control-system question

Figure: Useful audit telemetry records identity, provenance, canonical targets, policy decisions, effects, and rollback state below the conversation layer. Yield Signal Daily editorial diagram.

The first reaction in the r/Anthropic discussion was skepticism. Commenters asked whether the message was a scam, whether the screenshot had been altered, and whether Korean won had been mistaken for US dollars. That caution was reasonable: a dramatic payment email should be treated as unverified until the merchant domain, card activity, and account ledger agree.

After reports of the bank attempt and Anthropic’s acknowledgement, the discussion shifted. “Vibe billing” became the joke, but the useful criticism was more concrete: why was there no hard ceiling, anomaly hold, or human review before an eight-figure consumer payment request reached the processor?

The community’s proposed bug explanations should not be treated as evidence. Its risk question should. A billing system serving individual developers already knows enough context to classify a $16.6 million reload as an extreme outlier. It should stop there even if every upstream field claims the request is valid.

The missing layer was not one more dashboard warning

Figure: A production agent encounters deterministic policy gates before an irreversible operation and an external stop control during execution. Yield Signal Daily editorial diagram.

A mature payment path should treat configuration as input, not authorization. If a stored reload amount says $16.6 million, the system still needs an independent policy layer that asks whether the amount is permitted for this account, consistent with measured usage, and within recent spending velocity.

A safer billing path reconciles usage and account state before a bounded reload controller can contact the payment processor. Figure: Yield Signal Daily.

Five controls matter here:

1. An account-class hard cap

Consumer and small-team accounts should have a non-bypassable maximum per reload and per day. Raising it should require explicit re-authentication and, beyond a high-risk threshold, human approval. A user-configurable budget is useful; a provider-enforced maximum is a separate control.

2. Ledger-to-dashboard reconciliation

The balance shown to the customer should be derived from, or continuously reconciled against, the same authoritative ledger used to authorize payment. A dashboard displaying $0 while a processor sees an eight-figure request is exactly the kind of disagreement that should open a circuit breaker.

3. Amount and velocity anomaly detection

An amount thousands of times larger than an account’s normal purchase needs a hold, not another retry. The rule does not require machine learning. Simple limits based on account history, plan type, recent usage, and percentage change would catch the obvious case.

4. Idempotent retries with a retry budget

Payment retries need a stable idempotency key, a bounded schedule, and a terminal state. Repeatedly presenting an invalid amount can trigger fraud controls, block a card, and turn a harmless decline into a real operational incident for the customer.

5. Risk-based support escalation

An eight-figure attempted payment should bypass ordinary chatbot queues. The event already contains the severity signal: merchant-confirmed attempt, abnormal amount, and payment failure. A human billing specialist should receive the ledger snapshot, processor response, and account configuration before the customer has to reconstruct them.

What AI developers should change today

Anthropic’s official billing guide describes prepaid API credits and an optional auto-reload that purchases more credits when the balance falls below a threshold. That is convenient for production workloads, but it makes billing configuration part of the system’s operational risk.

Teams using any metered AI API should add controls outside the provider dashboard:

- Set auto-reload to the smallest amount that can survive a normal traffic spike.

- Use provider budgets and alerts, but mirror usage into independent telemetry.

- Put production keys in a dedicated organization or project with narrow permissions.

- Apply per-agent and per-workflow token, request, and dollar limits.

- Use a separate payment method with transaction alerts and an appropriate credit limit.

- Maintain a kill switch that can revoke keys and stop scheduled workloads without opening the vendor console.

- Reconcile invoices against request logs instead of accepting the dashboard total as the only ledger.

These measures cannot correct a provider-side payment error, but they reduce ambiguity. When a bill jumps, the operator can prove what ran, which credential was used, and what the application authorized.

The larger AI infrastructure lesson

The incident is not evidence that Claude secretly consumed $16.6 million of compute, and it is not evidence that an AI model wrote Anthropic’s billing code. It is evidence that the less glamorous systems around AI products deserve the same adversarial testing as the models.

Agent platforms encourage developers to automate long-running jobs, delegate tool calls, and scale requests faster than a human can watch them. That increases the need for deterministic boundaries around money. The model can propose work; a policy engine should limit spend. A configuration can request reload; an independent authorization layer should decide whether the payment is sane.

Anthropic says it corrected the auto-reload state after the bank rejected the invalid request. That did not undo the downstream card disruption reported by the user. The bank’s decline appears to have been the final effective guardrail. For an AI infrastructure company, the stronger standard is simple: an obviously abnormal request should fail closed before it reaches the customer’s bank, and an incident of this size should reach a human before the customer has to search for one across 15 emails.

Sources

- Original incident thread from @remy_notes

- Four-day support and bank-impact follow-up from @remy_notes

- User’s assessment of the unresolved operational impact

- ZDNet Korea: Korean user receives 25 billion won payment request

- IBTimes UK: Anthropic acknowledges the billing error

- Anthropic Support: How Claude API billing and auto-reload work

- Reddit: Initial r/Anthropic discussion

- Reddit: Follow-up discussion after the reported acknowledgement